Turning Point Brands, Inc

Not investment advice. Do your own DD. I am a state school student for crying out loud.

Summary

Turning Point Brands (TPB) is a manufacturer, marketer, and distributor of consumer products in the OTP (other tobacco products) industry. Their products consist of staple brands, like Zig-Zag rolling papers and cigar wraps, Stokers chew and loose-leaf tobacco, a vapor products distribution business, and branded vape and cannabinoid products. TPB summarizes its business into three segments: 1) Zig-Zag Products, 2) Stoker’s, and 3) NewGen, which includes their branded vape and vape distribution vertical.

After a 25% price decline since February 2021, TPB slipped back to the same EBITDA multiple that they had back in 2018 despite new strategic initiatives that dramatically increase the company’s growth prospects. These include:

A plan to rapidly scale distribution of the TPB’s most profitable products, including Zig-Zag’s entry into e-commerce and dispensaries/headshops, which generate 10-15x the sales of regular channels.

Turnaround of the low-margin NewGen 3rd party distribution business, which barely breaks even, into a pipeline for high-margin proprietary products. This has the potential to add up to 8pts of gross margin to the segment and $20m+ in annual operating profit in a few years.

These factors will help TPB grow FCF in the low-to-mid teens for the next 4-5 years. Yet, trading at just 15x LTM FCF when adjusting for certain one-off expenses experienced in 2020 (see “Release of ~$10-$12m in 2020 PMTA Expenses on page 3), this growth potential is not priced into TPB’s shares).

In addition, TPB has two key competitive advantages which I believe are undervalued by the market. These include:

A demonstrated ability to allocate capital through strategic M&A in a way that builds long-term value for shareholders

A distribution network to more than 210,000 retail stores, 1.5m online customers, and 4,000 vape stores. Such a distribution network has allowed TPB to rapidly scale the growth of acquired brands and new product lines.

Operations

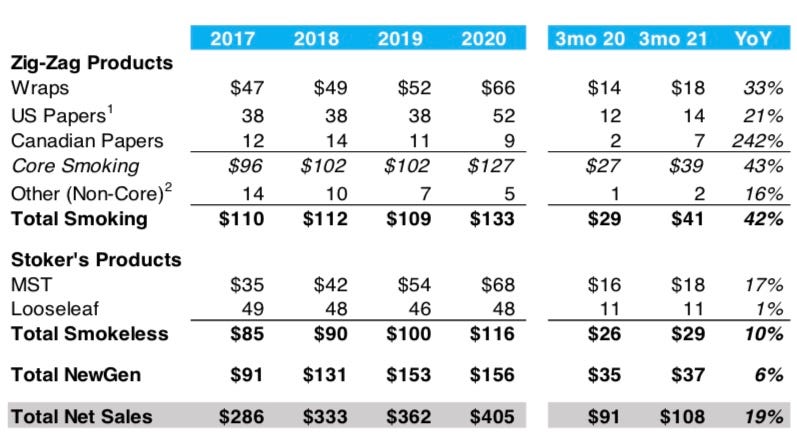

TPB has three segments, which I’ve summarized in the following table

Zig-Zag Products

Principal products include rolling papers and make-your-own cigar wraps. The Zig-Zag brand has been around since the late 1800s, but TPB acquired US distribution rights to Zig-Zag cigarette papers in 1992 under a 20-year contract, which was renewed in 2012, and automatically renews unless terminated by TPB or the licensor (see Appendix C “Licensee Risk”). TPB developed and owns the rights to their cigar wrap products. Up until 2020, sales of these products were stagnant until a new strategy was implemented by management to revamp the brand, move into e-commerce, and expand distribution.

Distributors choose to sell Zig-Zag products because of the quality of the product and the very recognizable brand with its iconic smoking Frenchman on the cover. This logo is popular among the youth; T-shirt’s bearing the Zig-Zag emblem are fairly popular on Amazon, which is something most rolling paper brands can’t brag about. Zig-Zag is often referred to as the “classic” rolling paper brand after over 100 years in the business. They developed a strong customer base in the United States with their papers cited as much easier to roll and much smoother than other papers.

Stoker’s Products

TPB manufactures, sells, and markets Stoker’s brand tobacco products. The Stoker’s segment includes moist-snuff tobacco (MST) and loose-leaf tobacco products. According to MSA reporting (MSAi), Stoker’s is the fastest-growing MST brand in the country, registering double-digit same-store sales and store growth. MST registers mid-60’s incremental margin for TPB and is around ~59% of segment sales. Distributors love this product because it seems to fly off the shelves whereas turnover is steadily declining for other smokeless tobacco products. The success is due to Stoker’s brand equity from 80 years in the chew business, and the perception of Stoker’s MST as a great value relative to price. Stoker’s offers retailers a tobacco product with brand recognition, a loyal user base, and boosts same-store sales.

NewGen

This segment contains leading wholesale B2B vape distribution platform, Vapor Beast®, and various B2C vape distribution platforms, including VaporFi, DirectVapor, and Vapor Supply. 3rd party product sales drive about 80% of the segment’s sales, at a ~30% gross margin. TPB made these acquisitions to build the infrastructure to launch proprietary products, which include the Solace vape brand and the Nu-X cannabinoid brand, which carry over a 50% margin. This segment also includes several other small ventures.

Below you will find a sales breakdown of each segment and each product.

Earnings Growth Catalysts

Release of ~$10-$12m in 2020 PMTA Expenses

In 2020, TPB spent $17m to get 250 products through the pre-market tobacco product application process (PMTA), which is a new requirement by the FDA for all tobacco products to be reviewed individually by the FDA before they can be sold. These expenditures, which were included in SG&A, will not continue in 2021, which will provide a nice $10m-$12m lift to earnings after-tax effects. On a base of $33m in after-tax earnings in 2020, this alone will increase earnings by over 1/3. This already manifested in Q1 2021, with quarterly SG&A expense down almost $3.5m. If we take these one-time expenditures out of LTM results, LTM FCF is around $56m, which at the current market cap of $850-880m, represents a trailing FCF multiple of 15-16x.

Distribution Expansion

Penetrating Cannabis Channels

TPB plans on adding their Zig-Zag rolling paper products to “alternative” sales channels, which include dispensaries and headshops in the US and Canada. The company began moving Zig-Zag products into Canadian dispensaries in 2020 and by 2021 they were in dispensaries covering 75% of the market. Sales in these stores have proven to be 10x-15x the sales that Zig-Zag products see in traditional retail stores, or about $10k-$14k in annualized sales per dispensary. The higher sales-per-store is attributable to 5-10x higher volumes on account of being in a specialized retail location, rather than a general store, and a higher average sales price per unit since dispensary sales carry a higher mix of their pre-rolled products, which sell for 4-10x the price of unrolled paper on a per-paper basis.

Such a high sales-per-store means sales will begin to scale rapidly and yield considerable operating leverage, since adding a few thousand more stores onto TPB’s network of 200,000+ stores likely won’t require hardly any capital or additions to fixed costs. At Zig-Zag’s 61% gross margin, I estimate that movement into just 4,000 dispensaries will add over $40m in revenue and $25m in incremental operating profit.

The US market remains hardly penetrated at all. Below is an example of the effect of adding 800 US dispensaries a year at $14k per store. Although, there is reason to believe that sales per store in the US could be much higher than in Canada since Zig-Zag has an established customer base and brand recognition in the US. Nevertheless, the figures below, and my operating model, use the modest assumptions of 800 US dispensaries added a year and $14k in sales per store.

*Assumes $14k in sales per dispensary, 800 new dispensaries a year, and a 61% gross margin

There are currently ~7,000 dispensaries in the US, with 6,000 of them in just 6 states. At a 15% growth rate for 5 years (less than the 20-30% growth projected by industry experts) there could be as many as 14,000 dispensaries. At just $10k in sales per dispensary, that’s $140m in sales potential (and $80m in incremental profits). While my model assumes the modest assumption of 800 US dispensaries added each year, I believe in the US they could penetrate over 1,000-2,000 US dispensaries a year for several reasons

They managed to add 700-900 stores per year in Canada, which is a country where they have little sales experience or brand recognition. This means TPB may be more efficient at adding dispensaries in the US than Canada.

With the purchase of VaporBeast in 2016, TPB gained distribution to over 4,000 alternative stores in the US, giving them a head start into the alternative channel.

Almost 5,000 of the 7,000 US dispensaries are in just 3 states, which minimizes any cross-state difficulties that could impede the speed at which TPB adds stores.

Continued consolidation of dispensaries will allow TPB to contract with hundreds or thousands of stores at once, similar to how they contract with c-stores. Right now, a few MSOs currently operate hundreds of dispensaries. However, as consolidation and industry growth continues, the largest MSOs will eventually operate thousands of dispensaries each, which will allow TPB to grow distribution rapidly at the rate of thousands of dispensaries a year which they can currently do with c-stores.

To summarize, TPB’s expansion into alternative channels doubled their addressable market and paves the way for a high growth rate of profitable sales by leveraging 10-15x higher sales and gross profit per store. This alone will lead to an additional $25-$40m in operating profit in 3-5 years, which is substantial compared to TPB’s consolidated $67m operating profit in 2020. If consolidation continues, sales and profits could scale even quicker.

Stoker’s Distribution Expansion

Growing revenues at over 20% a year, Stoker’s MST product is registering double-digit same-store sales growth AND distribution growth. TPB plans to increase the number of stores that sell their MST product by another 40-65%.

From Q1 2021 report

Turning Point Brands products are in about 210k stores as of Q1, with most of those being nationwide or regional chains. TPB’s relationships with these chains are what allows them to add MST products to 14k stores in the last two years and 36,000 stores in 5 years. At 7,000 stores a year, which is in line with their pace since 2015, distribution could grow by 35k stores in 5 years to 112k stores, which is a CAGR of 7.7%. TPB just spent ~$6m growing capacity at their production plants for MST, so I believe this growth is accomplishable.

Therefore, I think it is reasonable to expect 6-8% revenue growth for the next 5 years for MST from distribution expansion alone. If same-store sales simply keep up with inflation (which is a fraction of the double-digit same-store sales growth experienced), sales will grow in the 8-10% range for the next 5 years, with earnings likely to grow at a higher rate. If same-store sales growth is ~10%, then MST sales will grow in the high teens.

Lastly, MST carries a much higher margin than any of TPB’s products. Gross margin for MST is between 60% and 70%, while the gross margin for chew is in the 30s. This means segment income will likely outpace revenue growth as MST sales grow as a percentage of the mix, or low teens in the base case and high teens in the best case.

Zig-Zag Online Expansion

TPB was painfully late to the e-commerce party, having made Zig-Zag products available online for the first time in 2020. Since then, it has taken just one year for e-commerce sales to grow to a double-digit share of US Paper sales. US paper sales in 2020 grew 36% y/y, and it is reasonable to assume that a large chunk of the growth was due to e-commerce. There will be some cannibalization of Zig-Zag retail sales, but the move online introduces products to a much younger and wider audience and will overall be beneficial for Zig-Zag’s growth, as we saw in 2020 and Q1. Zig-Zag paper cones have over 3,000 reviews on Amazon, 90% of them 5-stars. While, this pales in comparison to their top competitor, RAW, which has 10s of thousands of reviews, I believe it still adds value to TPB’s business. E-commerce alone could provide 5-10% annual revenue growth for the US papers segment on top of the dispensary-related growth discussed above.

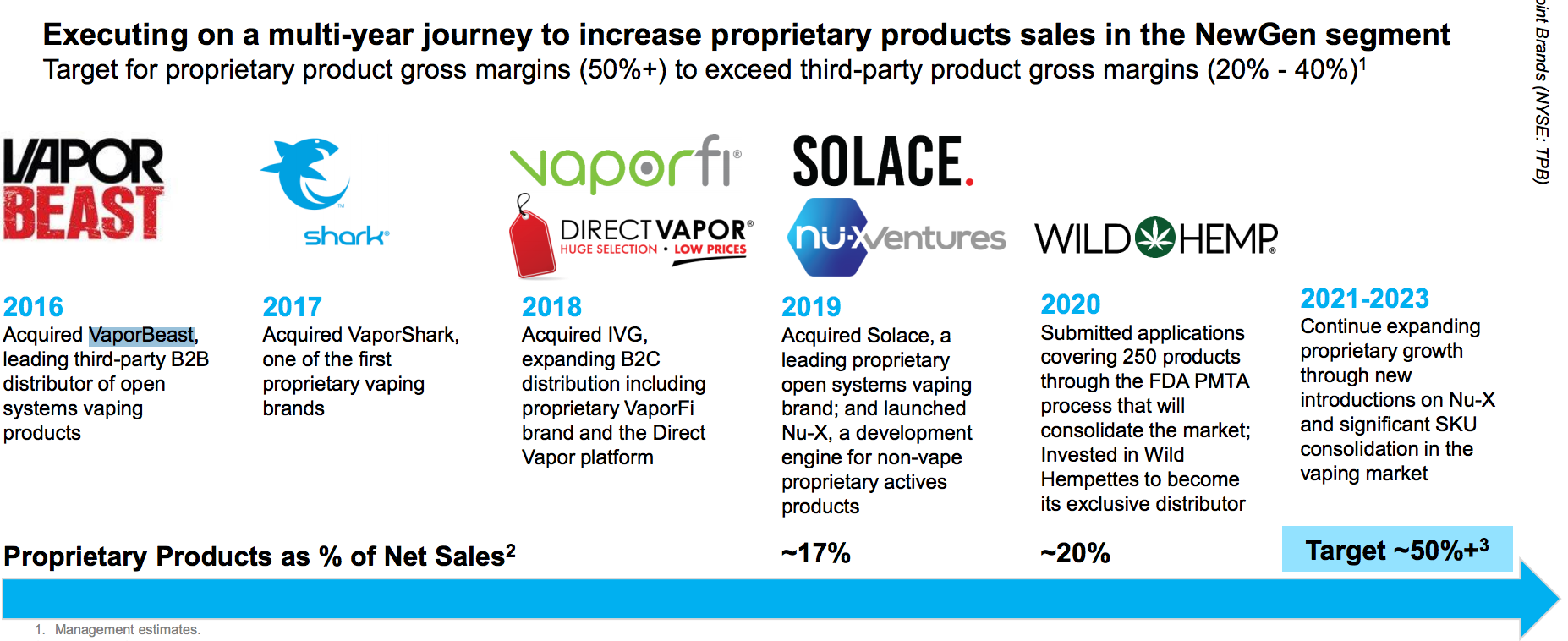

Turnaround of NewGen Segment

The market incorrectly assesses the value of the TPB’s NewGen segment. Perceived as low margin, high-competition business with significant regulatory hurdles, NewGen is actually on its way to becoming a much more profitable segment of TPB’s business with a stronger competitive position, on par with Zig-Zag and Stoker’s. The market fails to appreciate that this segment is a multi-year project to create a pipeline for scalable sales of high-margin proprietary cannabinoid and vape products. Moreover, with the passage of the Premarket Tobacco Product Application (PMTA) implemented by the FDA and the PACT legislation from congress, competition in this segment is going to sharply decrease.

An increased mix of High-Margin Proprietary Products

From 2016-2018, TPB spent $56m acquiring several vape and e-liquid 3rd party selling platforms, including VaporBeast and International Vapor Group, which included leading b2c vapor distribution platforms VaporFi and DirectVapor. These platforms saw $156m in sales, most of them 3rd party products. Management’s goal with these acquisitions has been to build up the distribution business through low margin 3rd party sales, and once that distribution channel has been established, to ramp up sales of proprietary brands. Right now, 80% of the revenue in this segment is from 3rd party sales, which carry a ~30% margin, while the other 20% is from selling proprietary products, which include Nu-X cannabinoid products (mostly CBD) and some vapor and hemp brands. TPB has acquired these brands and is plugging them into their distribution network, similar to how they built the Stoker’s segment. Proprietary sales carry over a 50% margin.

By 2023, TPB plans for high-margin proprietary products to represent over half of segment sales. Assuming the company can reach their 50-50 goal, gross margin would expand to around 40% (.5*.3 + .5*.5), up 7pts from 2020 levels, with continued margin expansion possible due to decreasing competition. This alone would add over $24m in annual operating profit in less than 5 years assuming no streamlining of the segment and just 2% annual revenue growth. TPB’s consolidated operating profit in 2020 was $64m.

TPB has demonstrated their ability to successfully build proprietary brands by plugging them into their distribution network (see “Undervalued Competitive Advantages”). After acquiring the distribution businesses, I believe TPB is positioned well to scale their proprietary products.

Increased Regulation Improving Competitive Position

There have been two critical regulations instituted by the FDA and Congress in the past year that will drastically reduce the amount of competition in the tobacco and vape industry. Those are:

The Premarket Tobacco Applications (PMTA)-- A requirement by the FDA for all tobacco products to be reviewed individually by the FDA before they can be sold. In each application, companies must provide scientific data that demonstrates a product is appropriate for the protection of public health.

The PACT Act -- Focuses on vape-product sales, and has several key components:

Ban on USPS shipping of vapor products.

Numerous record-keeping and tax requirements, including

Register with the ATF and the U.S. Attorney General

Register with state and local tax administrators in all states and localities where business is done

Collect and pay all applicable local and state taxes, and affix any required tax stamps to the products sold

Each month, a list of all transactions must be sent to each state’s tax administrator that includes the names and addresses of each customer sold to, the quantities and type of each product sold, and the name, address, and phone number of the person delivering the shipment to the recipient

Use private shipping services that collect an adult signature at the point of delivery

Verify the age of customers using a commercially available database

As a result of the PACT, all major private carriers like UPS, DHL, and FedEx stated they will no longer deliver vapor products due to the extra responsibilities. Amazon also recently took all vapor products off of their website. There has been one shipping carrier, simply known as 'X', who will provide vape and e-cigarette companies with the shipping services they need in 2021 and beyond. I imagine a few more non-major companies will rise to the challenge.

Both regulations will reduce the amount of competition to a large degree. Before, a company with a small R&D budget could whip up a product and use Amazon’s sales and fulfillment network to create a viable alternative to TPB and other tobacco companies’ products. Now, all products must go through the expensive and unappealing PMTA process, then they must find a site that can sell their product online that isn’t Amazon or compete for shelf space at brick-and-mortar locations. These new requirements mean new entrants will be very rare and those established players without scale, bargaining power, or a solid reputation in the industry will be severely weakened.

I believe these regulations prove beneficial for TPB’s business in the long-term for several reasons:

TPB has over $50m in annual FCF from two legacy segments to fund the transition to the new environment. Small players hemorrhaging money do not have this advantage.

TPB already has products in 210,000 stores and VaporBeast gives them distribution to over 4,000 vape stores. This gives them a significant head start as brick-and-mortar becomes a much more critical channel for the vape industry.

TPB has sufficient bargaining power and reputation to get their foot in the door with shipping carriers, something many competitors do not have.

One thing is for sure: the now crowded vape space will become much more concentrated in several years. Those who make it through will see much less competition, greater pricing power, and protection from new entrants.

Undervalued Competitive Advantages

Strategic M&A + Distribution Muscle

TPB has demonstrated the ability to generate substantial ROI from both strategic acquisitions and what they call “plug-and-play” acquisitions, which is when they acquire a strong, underrepresented brand and plug it into their large distribution network. Here are some examples from recent years:

Acquired Stoker’s chewing tobacco brand for $23m

Expanded distribution and added new product lines.

Now does $116m in revenue and $47m in operating profit.

Acquired VaporBeast, International Vapor Group, Vapor Supply, and Solace for $64m. They are leading B2C and B2B distributors of liquid vapor products

Collectively does $156m in sales and provide product-to-market infrastructure push sell high-margin proprietary products that could surpass $20m in EBIT in the next several years

Acquired rights from Durfort for $47m. The company acquired co-ownership in the intellectual property rights of all of Durfort’s Homogenized Tobacco Leaf (“HTL”) cigar wraps and cones

Immediately added 580 basis points to Stoker’s gross margins and $7m in EBITDA and by eliminating royalty payments

Provides manufacturing flexibility

Acquired 50% of ReCreation Marketing for $4m a specialty marketing and distribution firm focused on building brands in the Canadian alternative smoking accessories, tobacco, and other alternative products categories.

Used ReCreation’s Canadian marketing expertise and distribution pipeline to put Zig-Zag products in 75% of all Canadian dispensaries in one year, leading to ~$9m in sales in two quarters, up 100% from the previous year.

Management has a demonstrated ability to generate high IRR’s via these strategic acquisitions, especially when they utilize their distribution muscle in the “plug-and-play” acquisitions. Moreover, their M&A activity indicates a long-term outlook. With NewGen, they took an unorthodox strategy for a brand company by building the infrastructure via M&A for their proprietary products that would be developed later. In doing so, they built a self-reliant and robust system that provides them with not just distribution, but a network to receive continuous feedback on products to allow them to hit the ground running with their brands.

I believe the market underprices TPB’s ability to generate value for shareholders through M&A. Only one of the company’s current segments existed 20 years ago, and after spending just $87m, they have added two segments, NewGen and Stoker’s, which now generate $272m in revenues and $50m in operating profit with plenty more room for growth. 78% of Stoker’s revenues have occurred after becoming a part of the TPB family. In purchasing TPB’s shares, one is also underwriting management’s ability to uncover small but valuable brands and turn them into material additions to the company.

Incremental Returns on Capital

Zig-Zag

Zig-Zag requires almost zero capital to operate since TPB outsources production of the papers and just focuses on selling them, similar to a Coca-Cola business model. From 2015-2020, there were zero capital expenditures for this segment.

Stoker’s

Stoker’s on the other hand, is owned and manufactured by TPB, so the company does invest in PP&E. Incremental returns for this segment are still very high. From 2015-2020, TPB spent $16.7m in capital expenditures and grew NOPAT by $19m, from ~$17m to ~$36m, implying a return on incremental invested capital of ~114% in that period. Incremental returns today are likely higher, as the margin on MST is ~30 points higher than chew (65-70% according to management, which implies mid 30’s margins for chew).

NewGen

Incremental returns are difficult to calculate for NewGen, since its is a start-up segment and the company is investing capital through both PP&E and M&A.

Most of this segment’s assets are inventory with little fixed-assets are low. The segment required just $3m in capital expenditures since 2015. Below are the statistics NewGen’s subsidiaries when TPB acquired them. This can provide a glimpse into the incrementals of the segment.

Working capital (mostly inventory): $10m

Fixed Assets (likely doesn’t include operating leases): $1.6m

Total Group Sales in year Acquired: $126m

Working capital is the largest capital requirement of the segment at 7.9% of sales, lets call it an even 20%. If capex is 2% of sales, NewGen would require a NOPAT margin of just 1.4% for an incremental ROC of 10% which is above the company’s cost of capital. At a NOPAT margin of just 5%, incremental ROC is 23%, well in excess of the company’s cost of capital. The segment reported a operating margin of 3.7% in 2020. With margin expansion on the way, I believe incremental ROC for the segment will be sufficiently high.

Risks

Inability to execute management’s goals

Failure to obtain a competitive hold in alternative channels, which would limit future growth (see Appendix A: “Competition”)

Inability to form competitive proprietary brands in NewGen

Licensing terms to limit the growth potential of Zig-Zag, potential lawsuits, etc. (see Appendix C: “Licensee Risk”)

Heavy Debt Load (see Appendix D “Financial Condition”)

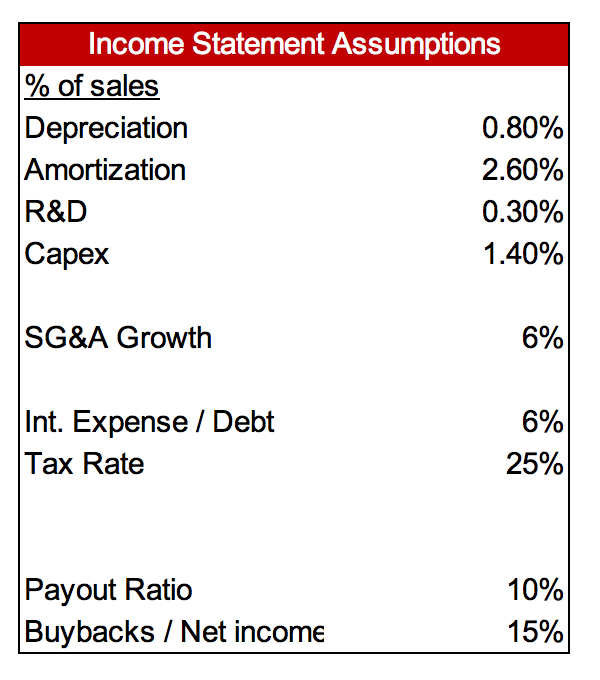

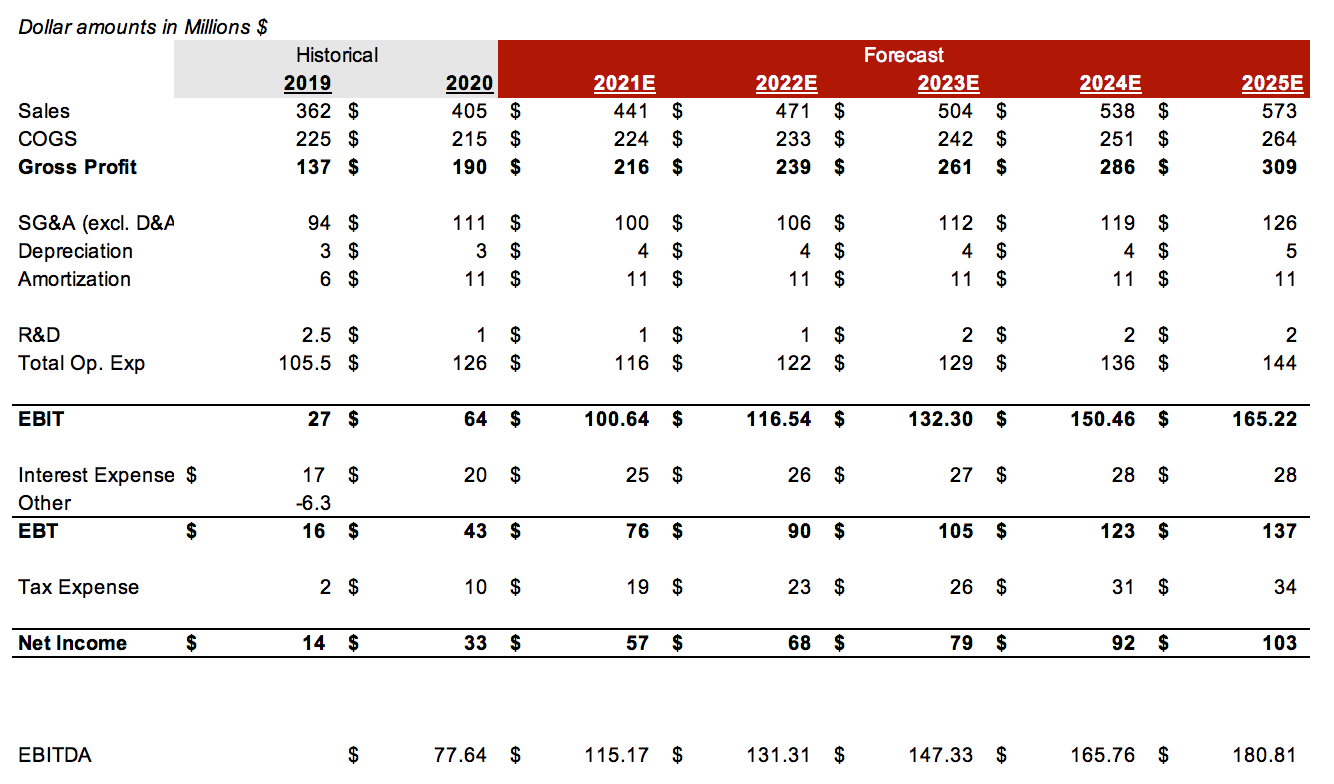

Operating Model & Valuation

Income Statement

Balance Sheet

Cash Flow Statement

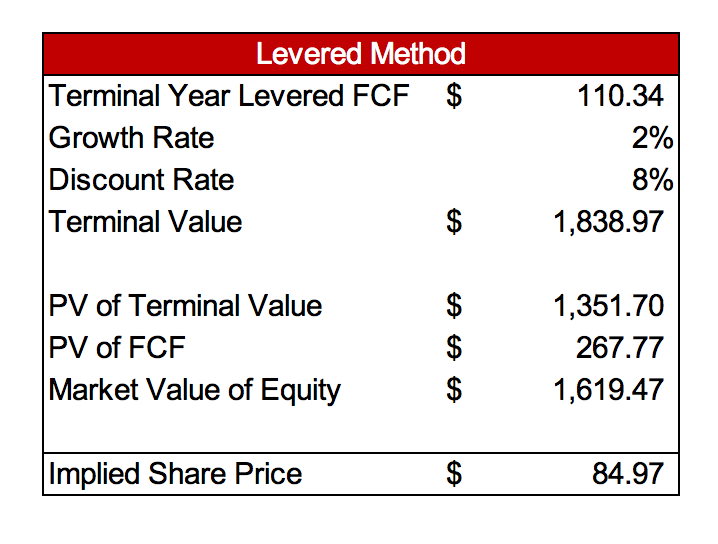

DCF Model

Appendix

A. Competition

Market Share

TPB’s reports market share figures for Zig-Zag and Stoker’s. However, these figures are only for “measured” channels, which don’t include stores like headshops and dispensaries. These alternative channels are estimated to be around 40% of the market, and Zig-Zag is just now moving into them. In the table below, I show TPB’s reported market share, which only includes the measured channel. Then, I estimated their share of the total market, first assuming 0% market share of alternative channels, then 5% of alternative channels. The difference is not material.

For Stoker’s most sales of moist-snuff tobacco and chewing tobacco occurs in traditional retail, so we can assume that these share figures are accurate. As of Q1 2021, Stoker’s has 25% of the chew market and 5.3% of the moist snuff tobacco market, up 300 and 50bps over the previous year, respectively.

Below are the y/y changes in market share for TPB’s key products in Q1 2021 for the measured channel. As you can, TPB’s competitive position in this channel is improving. However, if could include alternative channel sales, Zig-Zag’s share of the total market could have decreased.

Future

One of the biggest risks facing TPB is flopping in alternative channels. Since they missed the opportunity to get into these stores early, they have lost significant share to competitors like RAW, who have developed a loyal customer base. However, TPB doesn’t have to have the leading market share in these stores for the strategy to add value and growth. Look at Canada, where Zig-Zag has hardly any brand recognition or customer base, they managed to do 10-15x the sales in each dispensary as an average c-store. I would imagine they will have more success in the US, although I withhold such assumptions in this report.

For Stoker’s the story is different. They aren’t entering any new channels, so there is less uncertainty. They currently have a 5.3% market share in the total market and ~9% share in the stores where they actually sell products. I think we can expect consistent share statistics going into the future.

For NewGen, I already discussed why I think their competitive position will drastically improve in light of new regulations.

B. Management

I have highlighted management’s capital allocation abilities. However, there are also many ways that management has fallen short in the last decade. Failure to establish an online sales presence until 2020 is inexcusable. Even more irritating is the fact that they have barely penetrated alternative channels, despite the obvious value to a rolling paper company. Why would you not jump on these opportunities as soon as possible? It is almost as if they dismissed Zig-Zag as a declining cash cow and focused almost their energy on Stoker’s and NewGen. Despite these missteps, listening to earnings calls through 2020 and 2021 indicates that management has renewed confidence in the Zig-Zag brand, and they are now willing to invest in the brand.

To summarize, despite management’s mistake of neglecting the Zig-Zag brand, they have demonstrated the ability to create value for shareholders over time. With new strategic initiatives and a record of execution, I believe management will outperform expectations.

C. Licensee Risks

TPB does not own the trademark to Zig-Zag® brand premium cigarette papers. Instead, they have an exclusive distribution agreement with the owner Republic Technologies International (RTI). The license has existed since 1938 and has changed hands several times since then. have been exclusively licensed to us in the U.S. and Canada. Only about 50% of Zig-Zag sales are from the licensed products, the rest are sales of Zig-Zag products to which TPB owns the trademark.

The distribution agreement provides TPB will the exclusive right to market and sell Zig-Zag cigarette papers in the US and Canada. The Zig-Zag® trademark for e-cigarettes is also owned by RTI and has been exclusively licensed to TPB in the U.S. TPB owns the Zig-Zag® trademark for its use in connection with products made with tobacco including cigarettes, cigars, and MYO cigar wraps in the U.S. In subsequent years, TPB entered into two licensing agreements, giving TPB the exclusive use of the Zig-Zag® brand name for e-cigarettes and related accessories in the U.S. and paper cone products in the U.S. and Canada (collectively, the “License Agreements”). Each of the License Agreements terminates if the Distribution Agreements are terminated.

There are two primary risks that the licenses introduce into TPB’s business, 1) It could inhibit the growth of the Zig-Zag segment, as new products may have to be litigated with the licensor, and 2) tail risk if the distribution & license agreements are terminated. There are several ways in which that can happen.

Failure to meet performance obligations by either party

If TPB promotes cigarette paper or paper booklets of a competitor

The Licensor may terminate the Distribution Agreements if a competitor acquires a significant amount of TPB’s common stock or if one of TPB’s significant stockholders acquires a significant amount of one of TPB’s competitors.

In the event of termination, TPB is subject to a 5-year non-compete period.

There is nothing in the various licensing and distribution agreements that pose risk to growth catalysts already in place. TPB has attained the necessary licenses to distribute paper cones in the US and Canada, there is nothing preventing them from using e-commerce or putting products in dispensaries and headshops, and the company’s other segments are unaffected by such agreements since they own the necessary trademarks. Moreover, TPB has full pricing power over the licensed products they sell.

Nevertheless, the fact that TPB does not own the trademark to one of their key products certainly exposes the company to legal tail risk that puts $66m in profitable sales at risk. In addition, it can represent a barrier to innovation and reduces the company’s ability to act quickly when it comes to Zig-Zag, which is risky as the pace of disruption increases in the tobacco industry.

D. Financial Condition

Weighing on TPB’s valuation is their heavy debt load and low trailing interest coverage. Below is a table of the company’s debt.

This debt was used to fund acquisitions, primarily those associated with the $64m NewGen acquisitions and the $47m Durfort acquisition. With a cash position of $167m this puts net debt at around $255m. Net debt to LTM EBITDA is 3.1x, LTM EBITDA/Interest Expense of 4x, and Altman Z score of 2.4, which is on the lower side of what the market likes to see.

These statistics are trailing. With a concrete plan to bring the NewGen segment to profitability and expand the distribution of TPB’s most profitable products, I believe the market’s perception of TPB’s financial condition will drastically improve, leading to multiple expansion. Even if one is not confident in the NewGen transformation or the dispensary channel, earnings growth from Stoker’s expansion and e-commerce sales are fairly certain. Based simply on management’s 2021 guidance of ~$100m in EBITDA, up from LTM of $86m, we will soon see significant improvement in these ratios.

If this growth does not come, there is some assurance in that the company is very asset-light, only spending 1-2% of sales on capital expenditures, providing the company with sufficient flexibility to handle a decline in growth.

E. Sales-per-dispensary Calculation

TPB began moving products into Canadian dispensaries in 2020, which we can use to form reasonable expectations for results in the much larger US dispensary market. In Q1 2021, management stated that they were dispensaries that covered 75% of the Canadian market, which would be 700-900 dispensaries depending on the size of the dispensaries they are in. We know that in Q1, sales increased +$2.5m over the prior year (they actually increased $5m, but half of that was due to delayed shipments from Q4). This increase is entirely attributable to dispensary sales. That comes out to roughly $2,800-$3,600 in quarterly sales per dispensary, or $11k-$14k in annualized sales per dispensary. This is roughly 10-15x the sales Zig-Zag sees in each traditional store they are in. The higher sales-per-store is attributable to 5-10x higher volumes on account of being in a specialized retail location, rather than a general store, and a higher average sales price per unit since dispensary sales carry a higher mix of their pre-rolled products, which sell for 4-10x the price of unrolled paper on a per-paper basis. It is very likely that Zig-Zag could see higher sales per dispensary in the US, where they have a customer base and a recognized brand. However, I refrain from making such an assumption in my calculations.

F. Dilution

In Q1, TPB showed diluted shares outstanding of almost 22.7m, a 13% increase y/y. This was due to an accounting change requiring the dilutive effects of TPB’s convertible senior notes to be reflected in diluted EPS. These notes are convertible into 3,202,808 shares of voting common at approximately $53.86 per share. Luckily, there are several mitigants of this dilution.

First, the TPB purchased capped call options associated with the notes. This gives them the option to repurchase shares after notes are converted, offsetting the dilution. However, GAAP prevents TPB from reflecting the anti-dilutive effect of these capped call options in their diluted share count, therefore inflating the company’s diluted shares outstanding. TPB’s actual share count will not change due to the convertible notes. Below are quotes from the company’s filings regarding this provision:

“TPB purchased capped call options associated with the convertible notes for $20.5m. The capped call transactions have a strike price of $53.86 per and a cap price of $82.86 per, and are exercisable when, and if, the Convertible Senior Notes are converted.”

“This capped call transactions cover the same number of shares of common stock that initially underlie the Initial Notes, offsetting all the potential dilution of the convertible notes.”

In addition to these provisions, the bonds are redeemable after July 15th 2022 and when the stock price hits 130% of the conversion price ($70) for 20 trading days (doesn’t have to be consecutive).

As for additional dilution, TPB announced a $50m buyback program last year and repurchased $6m in stock in Q1 2021 $10m in 2020, with $34m remaining in the program to partially offsetting dilution. It is more than likely additional buyback purchases will be announced in the future, given TPB’s strong cash flows, and asset-light operating model, and management’s attraction to such repurchases.

**Disclosure: I have a long position in the above security**